DAVID CAY JOHNSTON . NY Times . 17 january 2002

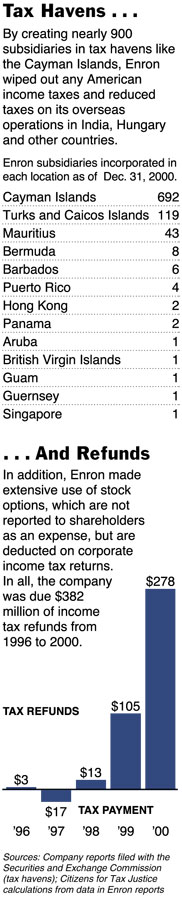

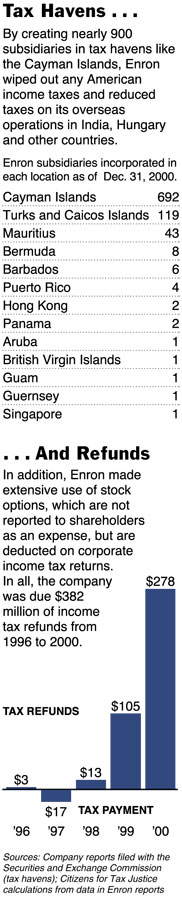

Enron (news/quote) paid no income taxes in four of the last five years, using almost 900 subsidiaries in tax-haven countries and other techniques, an analysis of its financial reports to shareholders shows. It was also eligible for $382 million in tax refunds.

The company used strategies common among businesses to avoid taxes. It also used some unusual methods, among them the creation of 881 subsidiaries abroad, including 692 in the Cayman Islands, 119 in the Turks and Caicos, 43 in Mauritius and 8 in Bermuda.

Two Enron subsidiaries have been accused by a group of insurers of engaging in sham transactions in a tax haven, according to papers in federal bankruptcy court in New York.

Enron is by no means alone in not paying income taxes. A small but growing percentage of large companies pay no income taxes, a study by Citizens for Tax Justice showed in October 2000. The study of half the Fortune 500 companies found that 24 owed no tax in 1998, up from 13 in 1997 and 16 in 1996.

While it is common for American companies to create subsidiaries in tax havens abroad, Enron had far more than most other companies, tax experts said.

Dynegy (news/quote), a Houston competitor of Enron in the energy trading business, said yesterday that it had no subsidiaries in tax havens. In disclosure reports, Chevron (news/quote) lists three subsidiaries in tax havens and Exxon Mobil (news/quote) lists six.

The tax-haven subsidiaries enabled Enron to create partnerships to eliminate taxes using techniques that came under attack from the Treasury Department and the Internal Revenue Service during the Clinton administration.

The basic technique involves having profits go to a partner not subject to American taxes, like a bank in a tax-haven country. The partner, after taking its fee, then returns the profits in a form that is recognized as not taxable by American law.

Enron avoided taxes for another big reason: deductions for stock options. When executives exercise stock options the company takes a deduction on its corporate income tax return equal to the profit realized by the executive, even though it is not required to show an expense on its profit-and-loss statement to shareholders. The benefits to the company can be great, particularly if a soaring stock price leads to the exercise of large numbers of options. That was true at Enron when its shares were soaring in 1998 through 2000.

It is not clear from Enron's financial reports how much the tax-haven operations reduced the company's taxes. But Enron did disclose that deductions for stock options alone turned what would have been a tax bill of $112 million in 2000 into a refund of $278 million.

Indeed, the company paid taxes in only one of the years from 1996 to 2000, while the government paid the company hundreds of millions of dollars in refunds.

The analysis of Enron's tax payments was performed by Citizens for Tax Justice, an organization that is backed by labor unions. But its calculations are widely accepted by groups with different views, like the conservative Heritage Foundation.

Mark Palmer, an Enron spokesman, said yesterday that he was unable to comment on the tax issues.

If shareholders had read just the large print in Enron's financial reports, they might have come away thinking the company did pay income taxes. The reports say the company paid hundreds of millions of dollars in corporate income taxes over the last five years. But company financial reports often disclose numbers different from what the companies actually pay because of such matters as when income is recognized and when expenses are deducted. So only in the fine print — the footnotes — of Enron's reports does it become clear that no tax was due.

Tax experts said corporations create offshore subsidiaries in tax havens for many legitimate reasons, including keeping profits earned overseas from being taxed in the United States, avoiding American regulation and insulating foreign business partners from American tax law.

These havens are also attractive because they do not require companies to disclose anything about their financial dealings.

"Their efforts to escape regulation and the tax issues are chicken-and- egg," said a former senior Treasury official who fought what he viewed as abusive corporate tax shelters, including one used by Enron, in the Clinton administration. He insisted on not being identified.

The official said Enron wanted to engage in trading far beyond what its financial resources would allow under the rules of regulators, from the Oregon Public Utilities Commission to the federal Commodity Futures Trading Commission.

Another way Enron reduced taxes was through a technique that allowed it to deduct interest payments to partners of subsidiaries. The Clinton administration unsuccessfully sought legislation to block that.

Enron used these and other techniques to eliminate taxes in other countries, several tax experts said.

"The object was to not pay taxes in any country where it operated," said one international tax lawyer who insisted he not be identified because he has worked on Enron matters.

"You certainly do not want to pay U.S. taxes on income earned in another country," he said. The lawyer was critical of Chevron and Exxon Mobil for not following Enron's example to avoid taxes, saying, "It is neither illegal nor unethical."

Donald C. Alexander, a former Internal Revenue Service commissioner, said that "partnerships are frequently used for the purpose of eliminating tax."

"You need a tax-exempt partner and so long as you can pass a fairly low threshold of substance it will work."

Enron has been a major lobbyist for exemptions from taxes and from oversight by regulatory authorities, spending $3.5 million in 1999 and 2000 alone on lobbying.

The chairman of the American Bar Association tax section, Richard Lipton, said the creation of hundreds of subsidiaries showed that Enron sought to "spread legal liability and reduce the possibility that if one partnership goes bad it will not infect any others." He said this would give comfort to other partners, like banks, dealing with Enron.

Mr. Lipton, a partnership specialist with the McDermott Will & Emery law firm in Chicago, said the existence of so many subsidiaries "raises only an eyebrow, not an alarm, but any allegation of shams raised by an insurance company is a red flag."

Just such an accusation is raised in filings by the Continental Casualty Company and other insurers in Enron's bankruptcy proceedings in New York. The insurers do not want to pay on bonds guaranteeing a deal involving Enron and two tax-haven companies. The insurers have refused to pay because they think the deal may be a sham, they say in their court papers.

In a court filing the insurers argued that the companies and Enron "may never have entered into any contracts with any end users" that were part of the deal and instead may have improperly diverted the money. The insurers had no comment.

Ronald A. Pearlman, a Georgetown University tax law professor, said it was likely that Enron wanted a new subsidiary for each of its many partnerships, but added that "the I.R.S. should be looking at these transactions."

Lee Sheppard, a New York lawyer who writes critiques for Tax Notes magazine,

said that "tax havens are also bank secrecy havens." She said

that given earlier disclosures about Enron executives' engaging in partnership

deals with their employer, "it may be that they were down there for

the bank secrecy and were just hiding things from shareholders, insurance

companies and partners, not just the I.R.S."

|

|